Alright. Go ahead and get comfy and… yeah, maybe grab a stiff drink (a Yoohoo, perhaps ;-)).

I’ve not written much recently. I am a music teacher, and our school started back in-person this past week, so most of my energy has been focused there. Also, the delay has also been due to my internal debate on whether I should post this article at all. Typically, the more an alarming alarmist alarms, the less people listen. The boy who cried wolf, as it were.

So, I’ll post this and then I’ll move on to other things. But, I pray you consider what is presented here, do your own research, and take the steps appropriate for your family.

What Prompted This Post

In my last article, Cryptocurrency: What It Is and Why I Purchased in 2020, I discussed the fiat money system and how the current endless printing of the US Federal Reserve Bank is causing inflation, which is a veritable tax on savings. Other central banks around the world are doing it, too. All fiat money is being debased.

However, over the past two weeks, disturbing things in the world of global finance have developed. I was not planning on writing anything on it because, frankly, doom and gloom really isn’t my style. But since there are practical positive responses to this information that might help at least one person out there, I figured it was time.

The impetus for this post was today’s video featuring Simon Dixon. Here’s a snippet from his bio on his LinkedIn page:

I’m an ex-investment banker turned Bitcoiner that left corporate in 2006 to work on my book on the future of banking. You will find me regularly quoted & appearing in much of the major press & media including BBC, FT, CNBC, Reuters, Bloomberg, Wall Street Journal to mention a few.

So, he’s not some conspiracy hack. He’s legit.

Here is the video he posted today:

The video Mr. Dixon is referencing here comes from the International Monetary Fund’s (IMF’s) website. You can find the video here.

What is Bretton Woods? And why does the IMF want something similar to happen again? I had no clue, so I found out.

Bretton Woods Conference, 1944

After World War II, the allied nations sent 730 delegates to the Mount Washington Hotel in Bretton Woods, New Hampshire. They were there to discuss how they could cooperate to prevent war and ensure economic benefits for all after seeing what happened after World War I and the factors that led to the march toward World War II. The now famous John Keynes (among economists, anyway) was the head of the United Kingdom’s delegation, and his macroeconomic philosophies loomed large at the conference.

The main outcome of this conference was the creation of the international monetary system that governed the world’s finances until the 1970s. Basically, every currency in the world had semi-fixed exchange rates against a reserve currency, the US dollar, which itself was backed by physical gold. Eventually, other countries like France started hoarding gold making it impossible for the US citizens or banks to redeem physical gold for US dollars; this prompted US President Nixon to decouple the US dollar from gold and instead made the dollar backed by trust in the government itself.

This move made growth explode around the world (since suddenly the total amount of “wealth” in the world could now be increased simply by printing more dollars). It allowed for cheap credit and thus mounting debt. While this system could theoretically work in perpetuity utilizing balanced budgets (ha) and other fiscally responsible measures (haha), humanity’s inclination toward excess combined with limitless debt potential would not end well…

The 2008 Crash and Calls for a “New Bretton Woods”

After the financial meltdown in 2008, which was partially due to a massive bubble in the US housing market, leaders from all over the world called for a new worldwide monetary policy. Dr. Zhou Xiaochuan of the People’s Bank of China called for a global reserve currency and a move off of the US dollar standard. After all, why should all the nations of the world suffer because of the monetary policy of one country?

This is known as the Trifflin dilemma.

One of the major problems with the original Bretton Woods system was (and is) the Trifflin dilemma. If one country’s currency is “the standard” to which everyone else’s currency is pegged, then that country (in this case, the US) will always have serious issues balancing the needs of its own populace with the economic demands of the rest of the world, including its enemies!

Foreseeing this issue, John Keynes proposed a global currency, unattached to any country’s monetary policies, and managed by a separate entity from any country. In 1944 at the Bretton Woods conference, the American delegation shot this down. After all, with World War II fresh on their minds and the USSR/communism lurking in the background as a rising global power, the Americans probably didn’t want the destiny of the US dollar in the hands of anyone but themselves. So they pushed for the US dollar itself to be the reserve standard, obviating the need for a single global currency.

But because of the untenable economic policies and never-ending spending of the United States (not just state, local and federal government, but also individual citizens and businesses too), confidence in the US dollar hit a new low in 2008, and then an even lower low in 2020.

Now, as Mr. Dixon has pointed out, the International Monetary Fund, created by the original Bretton Woods conference, has called for a revamping of the entire world economic system.

And this time, it looks like it’s going to happen.

It’s Different This Time

Below are several recent developments, unique in the history of mankind, that make this call for a new Bretton Woods moment carry much more weight than in the past.

1) Unique Setting in History

2020 has been a crazy year hasn’t it?

The pandemic, the most active Atlantic hurricane season in 100 years, social unrest around the world, an unprecedented Middle East peace process underway, insane fires and weather patterns in Brazil, North America, and Australia, seismic activity in North America, and… I mean, asteroids, man. Seriously, an asteroid on November 2nd, the day before the US election. Oy vey.

What else could possibly… eh, never mind.

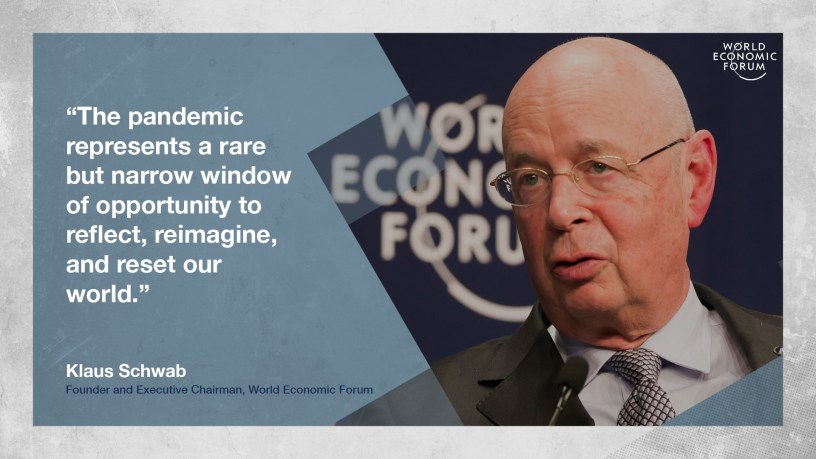

The point is, all these things have created a perfect opportunity for restructuring the global economy. The World Economic Forum actually has a name for it: The Great Reset. It’s not a secret.

For the first time, the technology exists to create a wholly different kind of society, one that won’t need physical cash/money. The Fourth Industrial Revolution, including robotics, artificial intelligence, 3-D printing, nanotechnology, quantum computing, and the Internet of Things, are dramatically changing every single industry around the globe. Even religion and philosophy (Is an AI a personal being or worthy of worship?) are being challenged and reconfigured.

2) Political Will and Public Awareness

The global pandemic, the shutdowns, and the resulting economic collapse has given political capital to world leaders who are interested in resetting the global financial system using an international reserve currency. And the public support is there for bailouts, with bills to be paid and children to feed if things go south.

Furthermore, there is so much turmoil around the world, particularly in the world’s economies, that people are actively looking for solutions on a global scale. Stimulus checks and the push toward Universal Basic Income (UBI) are seen as positives and are growing in popularity.

The interesting thing about enacting a UBI is, unlike before, there is now an easy and secure way to deliver monthly payments to everyone in the country and even the world:

Central Bank Digital Currencies, or CBDCs, and digital wallets.

3) Central Bank Digital Currencies (CBDCs)

I discussed cryptocurrencies in my previous blog post, but I did not talk about Central Bank Digital Currencies, or CBDCs.

CBDCs are not like cryptocurrencies as they do not rely on blockchain technology nor are they decentralized cryptocurrencies like Bitcoin. In fact, they are simply digital versions of fiat currencies (a la the US dollar).

The only difference between cash and CBDCs is while cash is mostly anonymous, digital CBDCs would be managed directly by the Central Bank that issues them. In other words, if you hold CBDCs, every transaction you make will be recorded in that Central Bank’s ledger.

With the adoption of CBDCs, the role of local banks or branches in the financial system would dramatically change. Your digital wallet will be a direct connection between you and your Central Bank, forcing your local bank to completely change its business model. Some might cheer this given the recent spate of bank fraud revelations.

While there are some positives to all of this (ie, any stimulus check you receive would bypass all banks and even the US Treasury and come straight to your digital wallet), the loss of privacy and autonomy for individuals are massive. central banks would become more powerful monetarily than any institution in their respective countries. Digital wallets managed by a central bank can be turned on or off by that bank; were this to happen, you would not be able to access your funds. Fantastic for fighting crime in that country, but not so great if you were the “wrong” ethnicity or religion (think of what China is doing to the Uighur Muslims).

And this isn’t pie in the sky, either. India started going cashless years ago. Multiple central banks are publicly working on CBDCs right now. The Ethereum blockchain can provide the platform necessary for CBDCs right now. The Bahamas is rolling their CBDC out October 20th, 2020! By the time you read this, this probably already happened.

4) Viable Candidates for Global Reserve Currency

The other interesting thing about all this is that, were a Bretton Woods-type conference held again, Keynes’ full vision about a global currency is now feasible. Let’s talk about XRP.

Ripple, a financial technology company based in San Fransisco (for now), has been maneuvering the cryptocurrency called XRP into position to be the only bridge currency for any and all remittance payments and currency exchanges anywhere in the world. So far, they are succeeding.

For instance, Ripple provides a service called On Demand Liquidity (ODL) to its customers (all of which are banks, financial institutions, and large multinational corporations). XRP, which has an open market value based on supply and demand, would be used by the ODL customers to record the transaction on its distributed ledger within seconds, ensuring that any currency to any party can be exchanged for any other currency, anywhere around the world. Currently, this same process takes days or even weeks to sort out using a complicated and cumbersome system of nostro and vostro accounts.

This all sounds very technical and whatever, I’m sure. 🙂

The point is, XRP’s blockchain is orders of magnitude faster and cheaper to run than Bitcoin’s. And it’s already being adopted and used by hundreds of financial institutions around the world; it has the capability and capacity to serve the world’s financial needs as a reserve currency should it ever replace the US dollar.

This is pie in the sky either, judging from this headline:

World Economic Form Names XRP As Crypto Asset Most Relevant in Central Bank Digital Currency Space

Interesting.

Get Outta Here With All Your Weird Money Stuff!

Yeah, I know. I totally get it.

I, too, want to just keep my head down, teach my music kids, be a good father and husband, and overall be a productive member of society. I’m sure you feel the same way.

But if all this goes down, you may find yourself having to make some hard decisions.

Practical Considerations for the Future

Like I said at the outset of this article, I am not looking to scare anybody or cause panic or anything. The world has been moving in this direction for almost one hundred years and all we can really control is our own actions and sometimes our immediate environment. That’s it. So there’s no point in getting worked up about any of this.

That being said, it’s important to think through hypotheticals like these and consider our responses beforehand in a non-emotional way. Then, if circumstances change, we will be better able to make rational decisions for what is best for our families.

- If the US dollar lost its reserve status, what would your savings or investments look like?

- If the US Federal Reserve decides that a digital dollar is the way to go, are you going to be willing to give up your privacy?

- If the Fed’s digital wallet was the only way to claim a stimulus checks or a Universal Basic Income, would you claim it? In March of 2020, both the US Senate and House of Representatives began working on this.

- Would you be willing to “turn in” your cash in exchange for the equivalent amount of CBDC? The United States did something similar in the 1930s when people were hoarding gold in order to maintain their savings during the Great Depression. The government forced them to sell their gold at below market value, making ownership of gold illegal. Australia did something similar in 1959 as well as the UK in 1966. I’m not saying this is going to happen; I’m just pointing out our shared history on the subject.

- If you want a peaceful way to opt-out of all of this, consider decentralized cryptocurrencies (Bitcoin, XRP, XLM, etc.). Here’s how I started: Crypto Casey’s beginner page. 🙂

- Also, consider Celsius Network (…or this link if you want me to make a couple bucks!) instead of a bank savings accounts to hold your cryptocurrency. Instead of making 0.1% APR interest rates like normal bank savings accounts, I make up to 11+% APR depending on the crypto!

Optional Homework

Check out the below videos if you want to know more.

God bless!